Choosing a reliable super fund is one of the most important investment decisions you’ll ever make. Because a super fund is typically a 40+ year investment, opting for a trustworthy superannuation fund that provides strong returns with the lowest-possible fees from the outset is the goal.

In this article:

Why the Right Super Fund Really Matters

There’s a very good reason why Albert Einstein (allegedly) called compound interest the ‘8th Wonder of the World’.

Here’s why:

Let’s say that you take $5000 every year for the next 40 years and invest it into an account with a 10% annual return. When you open that account in 40 years time you’ll be looking at a very respectable $2.78 million, with $2.58 million (92%) of that total sum being earned solely from interest.

Say you did the exact same thing again, but you mistakenly decide to invest in an account with a 7% annual return. In 40-years time you’ll be opening an account containing $1.14 million, a substantially smaller sum than if you’d decided to take the 10% return.

What seems to be a relatively small difference in fees or projected returns can actually make millions of dollars of impact over the long-term. That’s why choosing a great fund from the outset or switching to a better one right now, is a must for all Aussies who want to retire in comfort.

“Time in the market beats timing the market.”

How to Choose a Super Fund

When comparing different super funds, the main factors your need to assess are:

- Performance – It goes without saying but you want to actually look at a funds’ long-term track record to see whether it has a history of delivering high returns. Just because a fund has delivered high returns in the past doesn’t guarantee that you’ll get the same performance in the future, but it’s a good sign that the managers of the fund know what they’re doing.

- Fees – Fees are one area that can really differentiate a super fund. Very simply, you want to find the super fund that charges the lowest fees yet still provides the best management.

- Risk – When you’re picking a super fund you need to have a basic understanding of how much risk you want to take on. If you’re 19-years-old and just setting up a super fund for the first time, you probably want to go for a more aggressive strategy, because you’re not going to be affected by short-term fluctuations in price. If you’re 55 years-old however and you’re planning on retiring soon, you may want to move your super into a ‘conservative’ holding.

- Investment Options – Because a super fund is possibly the most long-term investment that any person will make, many Australians have sought to place their hard-earned money into super funds that support more ‘sustainable’ assets and industries. For example, Future Super is dedicated to investing solely in industries and companies that are “fossil fuel free”. When choosing a super fund, always look to see if the fund invests in assets you’re comfortable with.

Industry Funds Vs. Retail Funds

Before we get stuck into the best performing super funds, it’s really important to understand the difference between an industry super fund (remember those ads where people made the diamond shape with their hands) and a retail super fund.

Industry super funds were originally created by trade unions to provide money to their members when they retired, and they were typically only available to people working in specific industries. Over the years, however, most large industry funds have opened their doors to the general public, meaning that anyone can join. The most important part of an industry super fund is that they are not-for-profit, which means that all profits are returned to the members

A retail fund on the other hand is usually run by a bank, investment firm or some other type of financial institution. The key difference between retail and industry funds is that a retail funds is for-profit, meaning that all profits are distributed amongst the shareholders and not necessarily the members. Membership for retail funds is generally open to everyone, although some banks do provide incentives for customers to opt into their in-house funds.

The Best Super Funds in Australia (Actually)

At DMARGE, we understand how easy it can be for the marketing teams at different super funds to manipulate information and use flashy graphs to make their products look better than the others, even when it’s not remotely true.

That’s why we’re going to cut through the noise and use a range of different measurements to give you the best Australian super funds for your own needs. We’ll be assessing them on a variety of factors, from ‘benchmark outperformance’ over the past 7 years all the way to their performance on the Australian Prudential Regulation Authority’s (APRA) ‘Super Test’.

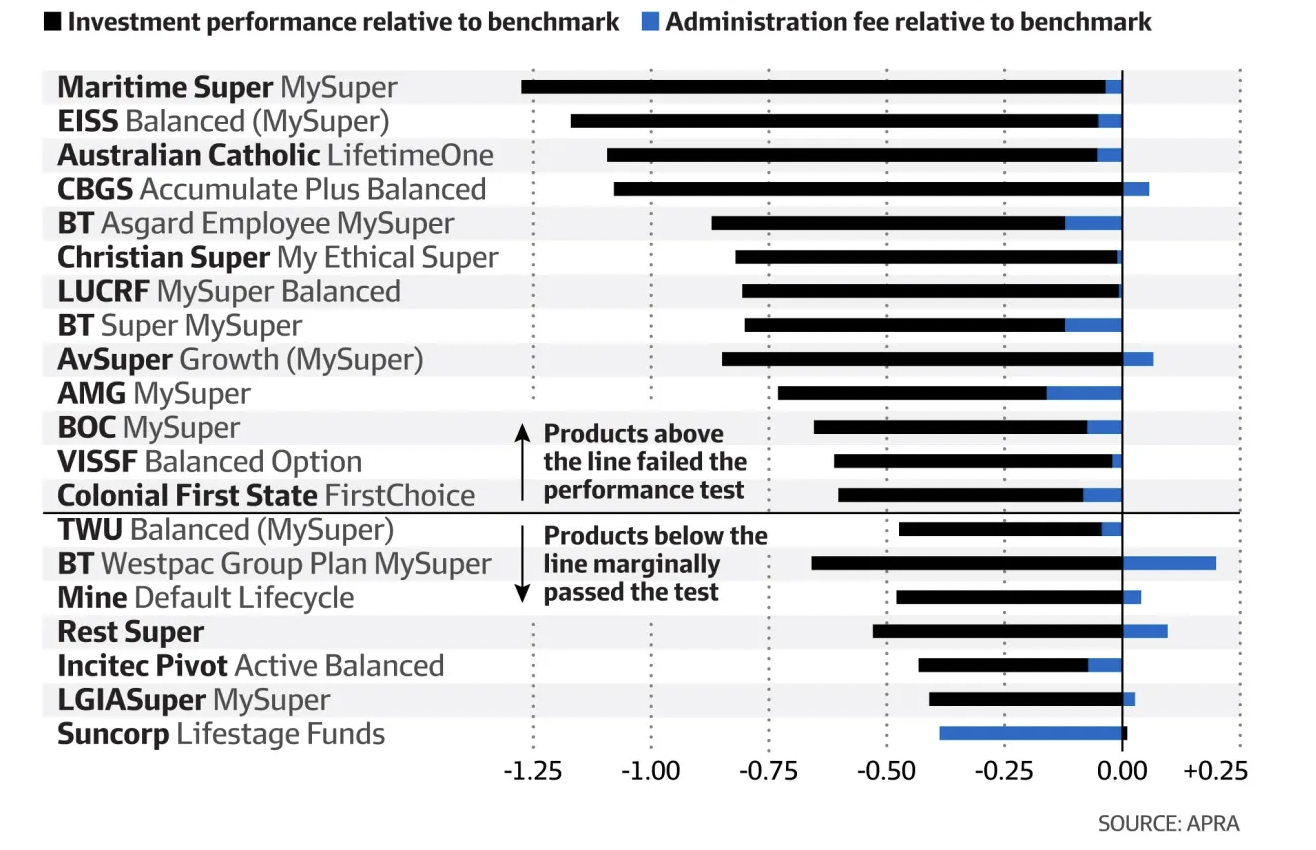

We’ll even throw in an added section called ‘The Dud-Funds’ where the unfortunate funds that fail APRA’s Super Test end up. If you’re holding your superannuation in one of the 13 funds listed in this section, it’s well worth switching over to a better alternative immediately.

Without further delay, here are the best super funds in Australia.

Best Performing Industry Super Fund: UniSuper

UniSuper was originally for those working at Australian universities (hence the name), but recently its doors were opened to the general public. Both Finder and APRA listed UniSuper as Australia’s best-performing industry super fund, with UniSuper offering 7 different investment options, ranging from very low risk to more risky, growth-oriented portfolios. UniSuper’s funds landed 4 out of the 10 top spots for the best choice of super in Australia, according to APRA.

UniSuper’s Balanced Fund was named as the best-performing default (moderate risk) fund overall in 2021, outperforming the super fund benchmark by 1.5% and delivering an average return of 9.22% over 7 years. The balanced fund also comes with extremely low fees, only charging $326 annually on a balance of $50k.

For younger investors, UniSuper’s High Growth Fund is one of Australia’s highest-performing super funds delivering holders an impressive 11.47% annually for the past 10 years and will only set you back $406 per year in fees on balance of $50k.

Best Ethical Fund: Australian Ethical

Australian Ethical is a superannuation fund that exclusively invests in companies that have a positive impact on the planet. Australian Ethical offers 7 different options that are risk-adjusted and focused to varying degrees on sustainability, clean energy, waste management, recycling, health and responsible banking. It actively divests from industries and assets that deal with coal, oil, tobacco and gambling.

Australian Ethical has one of the best performing long-term funds in the business, with its Balanced Fund returning an average of 9.01% for the past 10 years. It is worth noting that Australian Ethical does charge higher fees than competitors — the Balanced Fund will set you back $622 yearly on a balance of $50k.

Its more aggressive Australian Shares Fund is also one of the best performing super funds of the past 10 years, delivering an average of 14.01% annually to investors for the past decade. It is fairly costly with yearly fees coming to $842 on a balance of $50k and is aimed at investors with a higher tolerance for risk.

Strong Long-Term Performance: Aware Super

Aware Super is Australia’s second-largest super fund, currently managing around $130 billion in assets. It is also a not-for-profit industry fund with over 750,000 members. Aware provide a large selection of 12 different funds to choose from and boast some of the most steady long-term returns in the market.

Aware’s Balanced Growth fund has returned a respectable 8.97% for investors over the past decade and is mid-range when it comes to fees, charging around $519 a year on a balance of $50k.

Aware Super also has a specific ethical investment product called the ‘Diversified Socially Responsible Investment’, which is an investment option that excludes companies operating in the tobacco, ammunition, gambling, alcohol, forest logging and pornography industries, as well as companies that attribute 20% or more of their revenue to coal, oil and gas.

Despite not advertising themselves as an ethical super fund, AwareSuper actively tries to avoid association with tobacco companies across the board, only holding a total 0.1% exposure to tobacco across all of their portfolios.

Best Lifestage Fund: Virgin Money

While each super fund is different, they all invest in a variety of growth assets — such as shares and property, intermingled with defensive assets like bonds and cash that are less volatile. While shares and other growth assets can be subject to wild price swings, they tend to be much better investments over the long term. As you get older, you’ll have a bigger super balance and less time to ride out ups and downs in riskier investments like shares and property. It’s a time when it’s usually better to play things safe by choosing an option with a higher allocation of defensive assets.

This is why Virgin Australia’s Lifestage Tracker fund is a great option for someone looking to leave their finances running in the background, as it automatically decreases your risk exposure as you age.

The Lifestage Tracker fund is only 3 years old but has so far provided solid returns for holders, returning an average of 10.04% over the past 3 years. It also has one of the lowest fee-rates on the market, only charging $363 annually on a balance of $50k.The investment team at Virgin Australia were also named a Responsible Investment Leader 2020 and 2021 by the Responsible Investment Association Australasia (RISA).

Best New Fund: Spaceship

Spaceship is the new kid on the fund manager block, and it’s looking to the next generation of passive investors, having products for both superannuation and retail investing. Spaceship markets itself as a fund that actually invests in the future, specifically targeting 20 to 40 year olds and allocating a large portion of its holdings to high-growth tech stocks such as Tesla, PayPal and Shopify

Spaceship’s superannuation fund is definitely for younger investors that are only just getting started as the GrowthX Fund is highly allocated towards risky ‘growth’ assets, with around 30% of the funds total portfolio in US tech stocks. If that suits your risk tolerance, the GrowthX Fund is also one of the least expensive high growth funds in the market, only costing around $536 per year on a balance of $50k.

Spaceship also comes with a mobile app. The only major downside is that there are only two fairly high-risk superannuation products available at the time of writing, which means that those of you looking for more choice or a more conservative option are best to look elsewhere.

The Best Overall – AustralianSuper

Saving the best for last, the best overall super fund for Aussie investors is AustralianSuper.

It offers the widest range of strong-performing investment options so that investors can tailor a portfolio to their individual needs more easily. Australian Super has also routinely outperformed the benchmark of other Australian funds over the past 10 years, and also receiving one of APRA’s top spots in 2021.

It’s Balanced Fund received the Finder award for the best Australian super fund in 2021 and has been one of the strongest performing super funds of all time. The balanced fund has returned a strong 9.74% annually over the past 10 years and will only set you back $476 per year on a balance of $50k.

AustralianSuper is also one of Australia’s largest, most user-oriented funds, as it comes with its own mobile app and the website is clean and easy to navigate. AustralianSuper also makes sure that all documentation is pre-filled with your information as soon as you sign up, which takes the hassle out of filling out tax and super forms for yourself.

What About the Worst Funds?

What review would be complete with a good old-fashioned name and shame?

These are the super funds products that failed to meet the standards set by APRA. If a fund ends up on this list, it usually means that it’s charging absurd fees or that its overall performance is genuinely bad. If you see your fund here, take this as a sign to swap over to one of the funds mentioned above, or speak to a financial advisor about finding a new fund that will best suit your own unique financial circumstances.

- AMG MySuper

- ASGARD Employee MySuper

- Australian Catholic Super: LifetimeOne

- AvSuperGrowth: MySuper

- BOC MySuper

- Christian Super: ‘My Ethical Super’

- FirstChoice Employee Super

- Commonwealth Bank: ‘Accumulate Plus Balanced’

- Energy Industries: Balanced (MySuper)

- Labour Union Retirement Fund: MySuper Balanced

- Maritime Super

- Retirement Wrap: BT Super MySuper

- VISSF Balanced Option

Read Next: